Mobile money channels

In the previous topic, we discussed the history of mobile money and how it came to be. Now you’re probably wondering how someone would practically make use of the mobile money ecosystem.

Let’s start by discussing how users can access the ecosystem.

In traditional banking, you would typically access the money in your account via an ATM, debit or credit card, internet banking website or mobile banking app. Similarly, the mobile money ecosystem provides various channels to access the system. In this topic, we will cover a few of the most commonly used channels including the USSD, mobile application, web portal, hosted payment page, API, and physical channels.

")

USSD channel

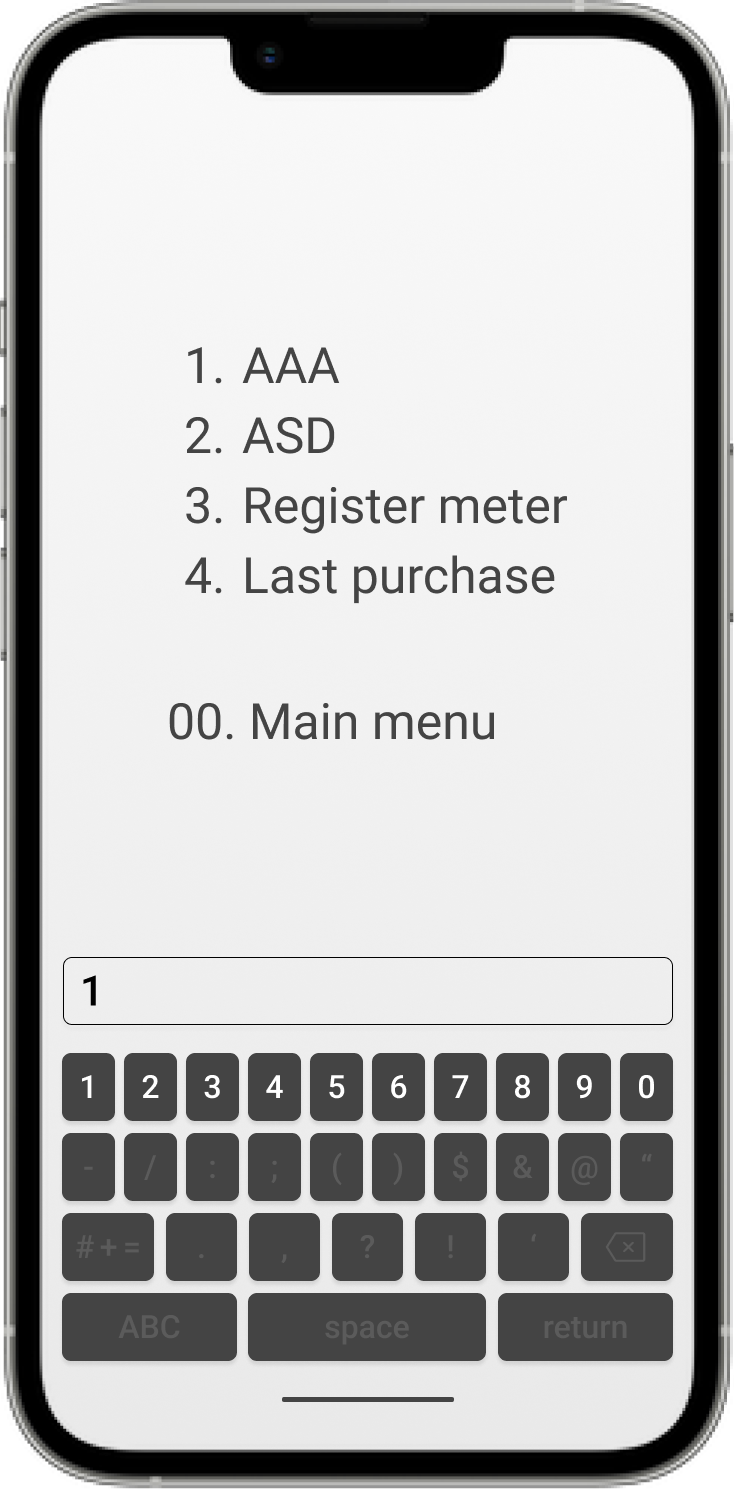

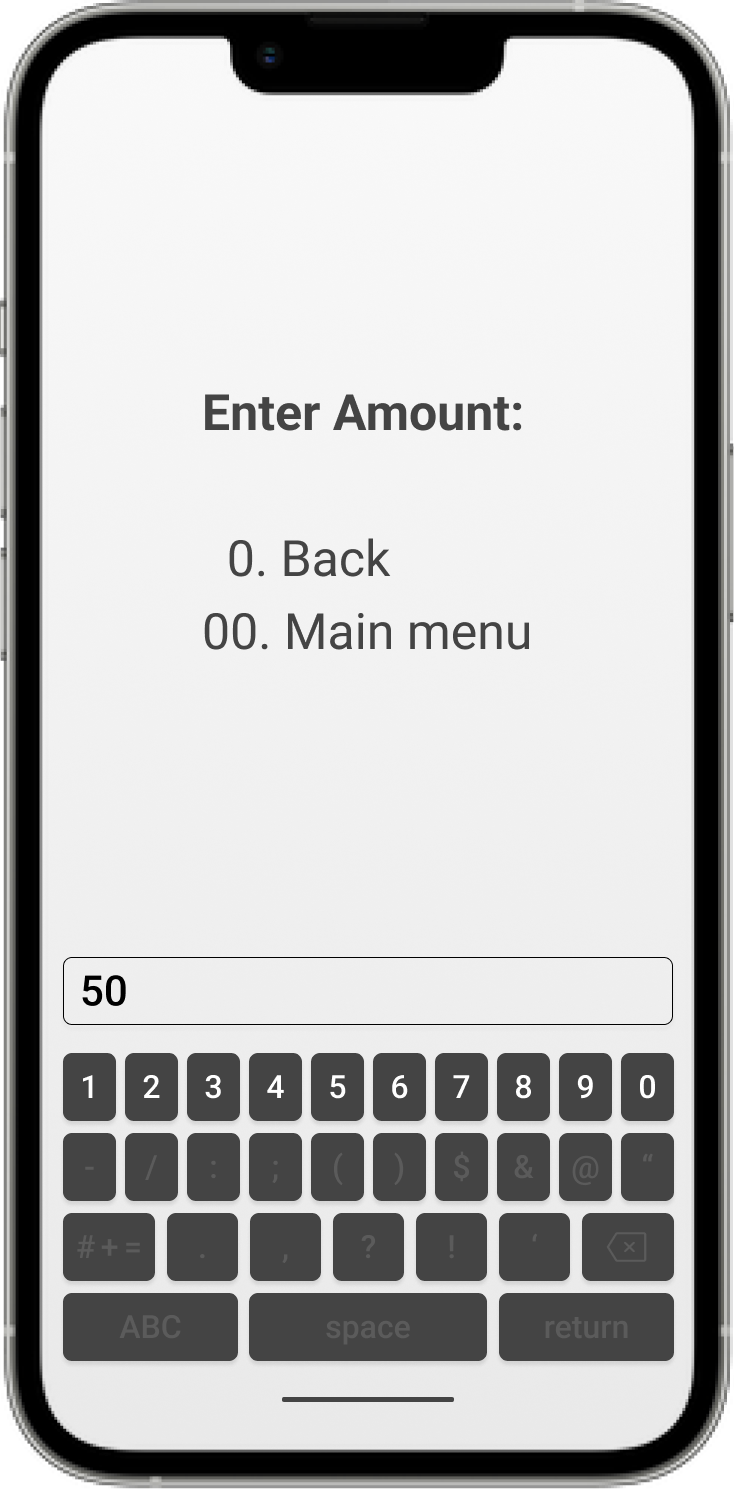

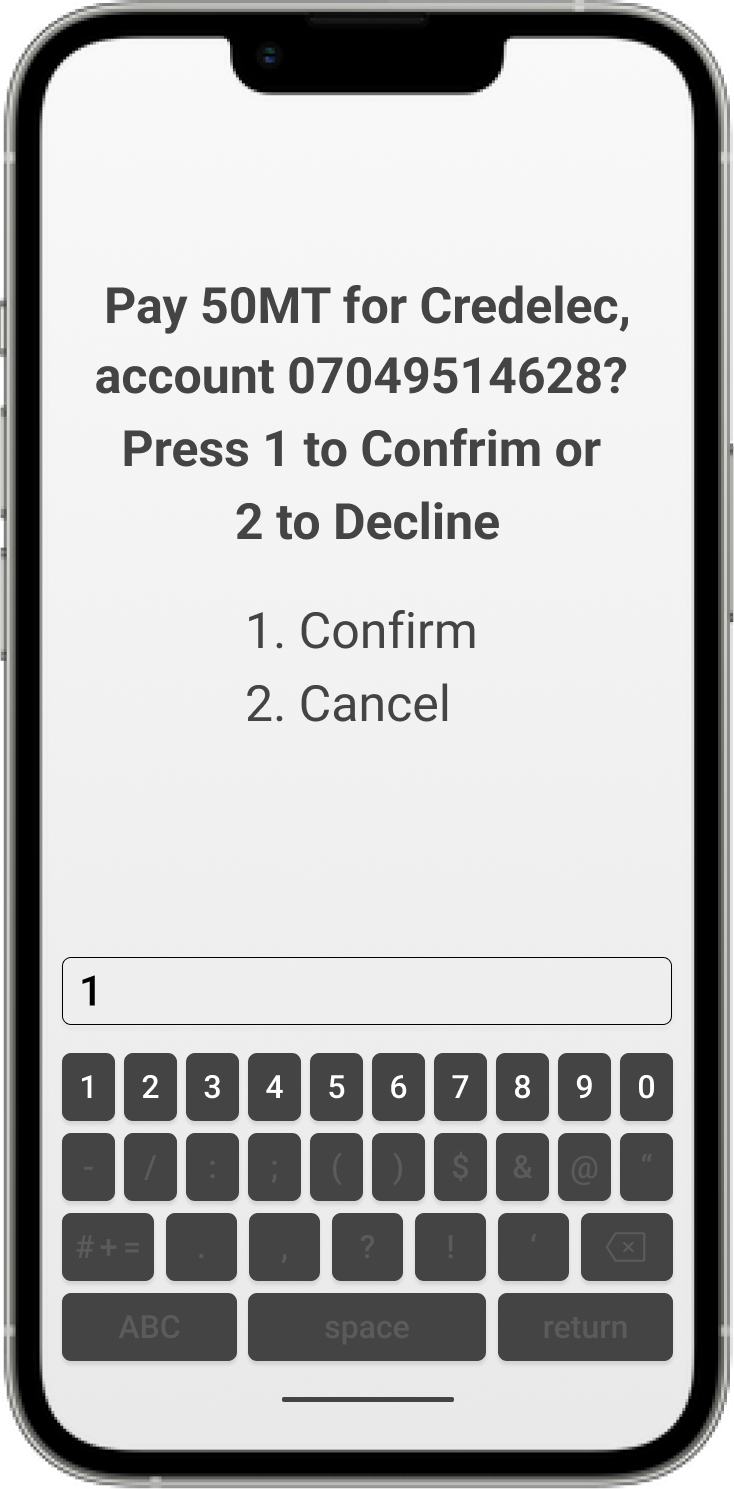

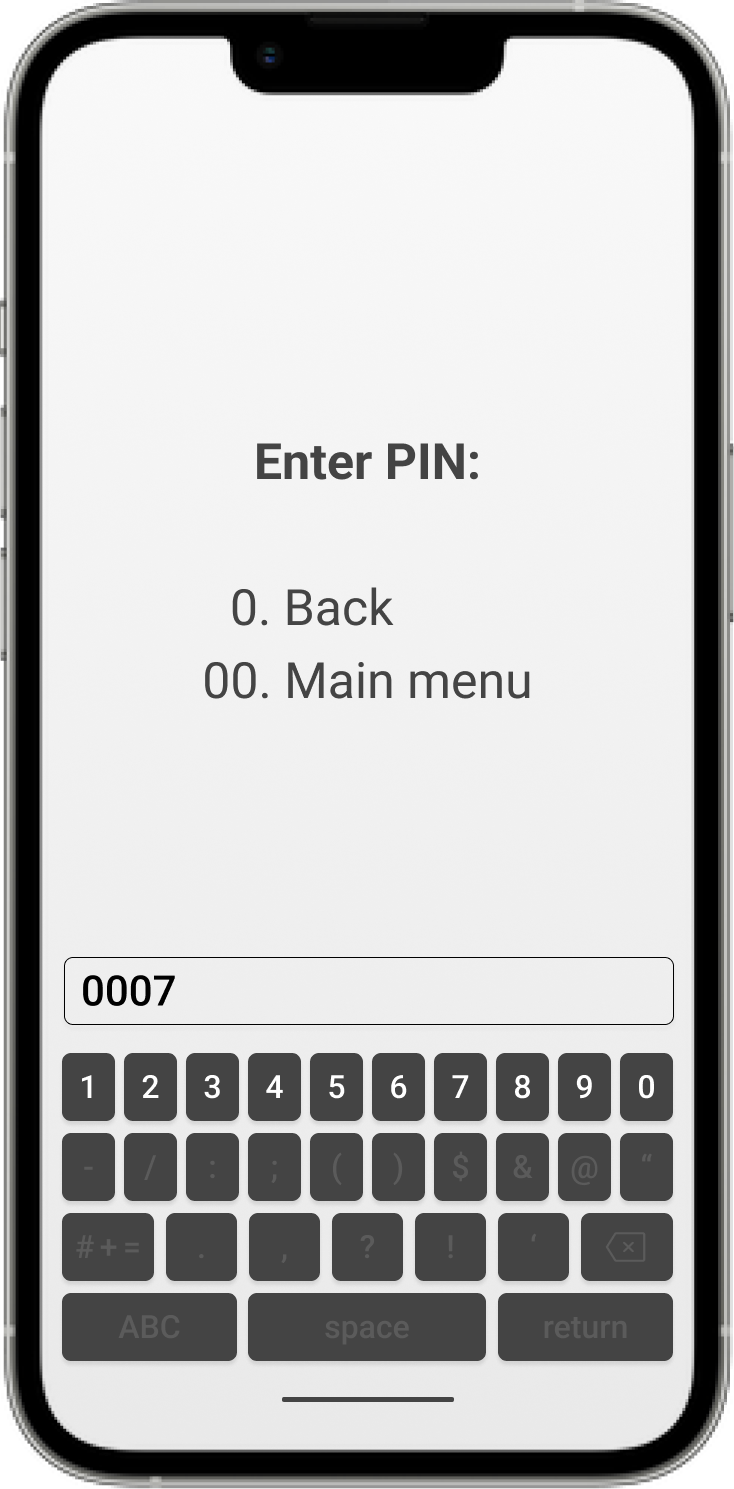

The first and most popular channel is the USSD channel, which allows mobile money operators to interact with users using short codes. You might be familiar with these short codes, such as *100# or *121#, which are commonly used to check your airtime balances, and buy airtime or data bundles.

You can go ahead and try typing one of these short codes on your mobile device to see a real-life example of a USSD menu. We have also created a screenshot slideshow for you below. Just click through the images to see the user journey.

Typically, the mobile money operator will assign a specific USSD short code to their mobile money service. When a registered mobile money user enters that short code on their mobile device, they are presented with a menu containing a list of options available to them on the mobile money service.

For example, a user could choose to check their mobile money balance, send money to a friend, or pay for goods and services. Depending on the choice they make, there will be a series of follow up interactions. If, for example, they choose to send money, they will need to enter the mobile number of the person they are sending it to, and indicate the amount to be sent.

While very popular, the USSD channel does limit the user experience as it is restricted to a set of text-based questions and the user’s responses to them.

Mobile application channel

The second channel we will discuss is the mobile application channel. This channel is growing in popularity as smartphone penetration increases, and we are seeing more and more mobile money operators building their own mobile money mobile apps, which are similar to traditional banking apps.

Registered users with smartphones can download the application from their app store, install it on their iOS or Android device, and log in to access their mobile money account. While this provides similar functionality to the USSD channel, the user experience is enriched because there is much more versatility in what you can show the user and how you can show it.

Web portal channel

The third channel is the web portal, or website, channel. In this case, the mobile money operator creates a web portal that provides access to the mobile money environment via an internet browser. This is very similar to how you would log into your bank’s online banking website.

At the moment, this is a much less popular channel than both the USSD and mobile application channels.

Hosted payment page (HPP) channel

The fourth channel that we will cover, is the hosted payment page, or HPP. This is very similar to the web portal channel but with a few key differences.

An HPP is a web page that is developed and hosted by the mobile money operator and then embedded into a third party’s website. This is similar to what companies like PayPal have done, and allows users to make purchases on international websites like Amazon using mobile money.

")

Let’s take a look at an example. Let’s say John wants to buy a new game on the Play Store for $10. While many of you would use a credit card to do this, most people in developing countries, particularly those where mobile money is widely adopted, would not. So how does he pay for his game?

If the third party, in the case the Play Store, has embedded the mobile money operator’s HPP on their web page, John will see a payment option to pay with mobile money.

When he selects this option, the Play Store will redirect to the embedded HPP where he can enter certain information, such as his mobile number, to initiate the transaction.

It is important that only the mobile money operator handles John’s PIN, and not the Play Store. Therefore, the mobile money operator sends a request to John to enter his PIN before the transaction can be completed.

API channel

The fifth channel we will discuss is the API channel, which is typically used for machine-to-machine communication. In other words, it is used when an external system wants to automatically perform transactions on the mobile money ecosystem without human intervention.

Let’s say there is a business that wants to automatically make their monthly salary payments on the mobile money ecosystem. In this case, the business would integrate their payroll system with the mobile money API channel to allow the system to automatically communicate with the mobile money ecosystem on pay day.

Physical channel

The sixth, and final, channel we are going to discuss is the physical channel, which typically involves an agent.

For example, a customer could physically hand cash to an agent who then adds the equivalent value of EMoney to their mobile money account. Similarly, an agent could deposit cash at a physical bank, and the equivalent value of EMoney will be added to their mobile money account.

Although our systems aren’t typically involved in this channel, it is important to understand that it still represents a way for customers and agents to access the mobile money ecosystem.

Summary

So to summarise, users can access the mobile money ecosystem in many ways. We have covered six of these channels namely USSD, mobile applications, web portals, hosted payment pages, APIs, and physical interactions.

USSD is the most popular of these. While it is a relatively old technology, it is still used extensively across Africa for three main reasons:

- Feature phones are much more common than smartphones, which have relatively low penetration levels compared with the rest of the world.

- USSD is a free service, so Users don’t need to pay for data usage or SMSes.

- Users don’t require 3G or 5G reception to access USSD services.

In the next topic, we will look at who can access the mobile money ecosystem and the types of actions they can perform.